If I had known better, I could have helped my kids retire with $1 million in their retirement accounts, according to personal finance reporter Venessa Wong. She wrote about this idea in a Marketwatch article last week, and actually mentioned three ways that I could have helped… if I had known better.

But Ms. Wong didn’t think up these ideas herself. She heard them in a podcast called “The Money Guy Show” hosted by financial planners Brian Preston and Bo Hanson.

Pretty simple ways, really. And one of the ways captured my imagination.

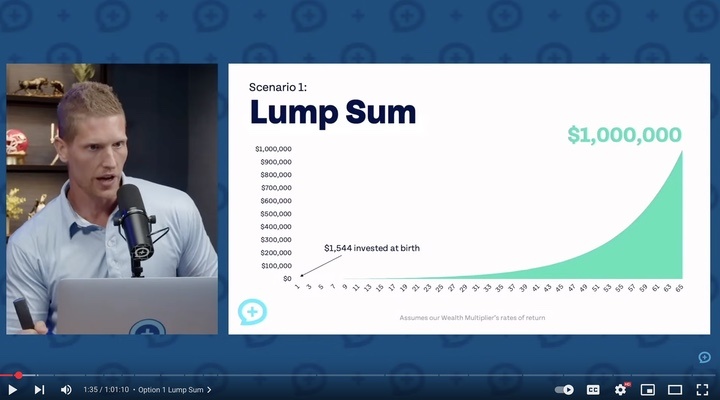

Here’s a graph by The Money Guys.

So simple. Invest $1,544 on the day your new baby is born, and never add another penny… and when your baby reaches age 65 and is no longer a baby, they will have $1 million in their retirement account, courtesy of the wonderful thing known as ‘compound interest’.

If only I had known about this when my kids were born. And even more depressing… if only my parents had known about this, when I was born. I coulda been rich.

Okay, that’s all water under the bridge. My parents screwed up, and so did I, and my kids will probably screw up if they ever have children. But that doesn’t mean the readers of this column need to screw up!

As Vice President JD Vance reminded us back in January, at the March for Life: we need more babies, and those babies need to grow up to be happy millionaires when they retire.

Our society has failed to recognize the obligation that one generation has to another, is a core part of living in a society to begin with. So let me say, very simply, I want more babies in the United States of America.

The Marchers for Life cheered loudly and enthusiastically.

I want more happy children in our country. And I want beautiful young men and women who are eager to welcome them into the world and eager to raise them.

And it’s the task of our government to make it easier for young moms and dads to afford to have kids, to bring them into the world, and to welcome them as the blessings that we know they are…

The Vice President didn’t exactly tell those young moms and dads to invest $1,544 into a retirement account for their babies, but I think that was implied, considering the problems with an insolvent Social Security system, and also with the cuts to SNAP food programs and Medicaid help for pregnant women. We all want to more happy children and it’s the task of government to make that affordable, but only if you’re already a billionaire.

My kids don’t always listen to my advice — and I don’t blame them for that, because they’ve watched how my life has turned out. But part of how my life has turned out was because I didn’t listen to my parents. And because my parents didn’t invest $1,544 when I was born.

Also, my kids don’t typically listen to advice coming from people like JD Vance. And I don’t blame them for that, either.

But should we listen to “The Money Guys”? Venessa Wong listened to them, and she noted:

The strategies outlined by Preston and Hanson assume aggressive growth — and require an extreme level of patience. Parents must start investing for their children as soon as possible, and the children must allow that money to grow, untouched, for five to six decades, leaning on the power of compound growth to gradually get to $1 million…

“This approach depends entirely on staying invested through multiple recessions, wars, bubbles and panics,” Christopher Haigh, a financial planner and co-founder of Iconoclastic Capital…

Does anyone honestly believe their kids will leave all that money untouched for 65 years? Through multiple recessions and possible foreclosures and student debt and — worst of all — the need to invest $1,544 into their babies’ accounts? The temptation to make an early withdrawal would be hard to resist.

Meanwhile, Ms. Wong was careful to remind us that, 65 years from now — due to the magic of inflation — $1 million will likely be enough money to buy a used car in good condition.

“The Money Guys” give out free advice on YouTube, hoping that we will click through to their website and buy their books. As we all know, free advice costs nothing, and it’s worth the price.

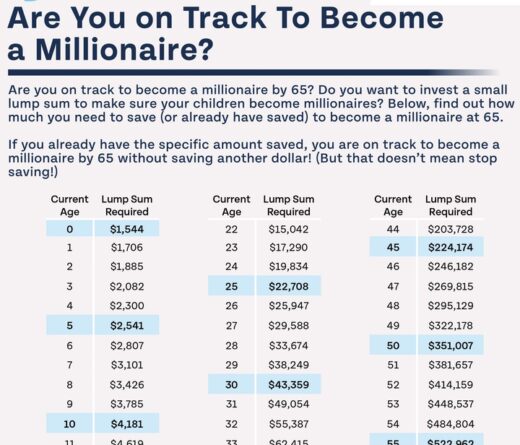

When I visited the “Money Guys” website — not to buy their books, but to learn more about how my parents had let me down — I found that they had published a careful list of how much you would have to invest in your children’s future, at various ages. At birth, the amount was $1,544 to let them retire with $1 million, but if you waited until your kid was 10 years old before investing, it would set you back $4,181. Which is nearly a year’s salary for a journalist.

If you waited until you were 61 (which is exactly what I have done) you would have to invest $790,238 if you wanted to retire with a million dollars at age 65. So obviously that’s not going to happen.

One thing that was not clear to me was where, exactly, we must invest this money. Should we invest in the stock market? Like, in the U.S. stock market?

Or should we invest in the Chinese stock market?

Because 65 years from now, financial investments are going to look really different than they do in 2025. At the rate things are going.

Underrated writer Louis Cannon grew up in the vast American West, although his ex-wife, given the slightest opportunity, will deny that he ever grew up at all. You can read more stories on his Substack account.