This op-ed appeared on StrongTowns.org on August 19, 2024.

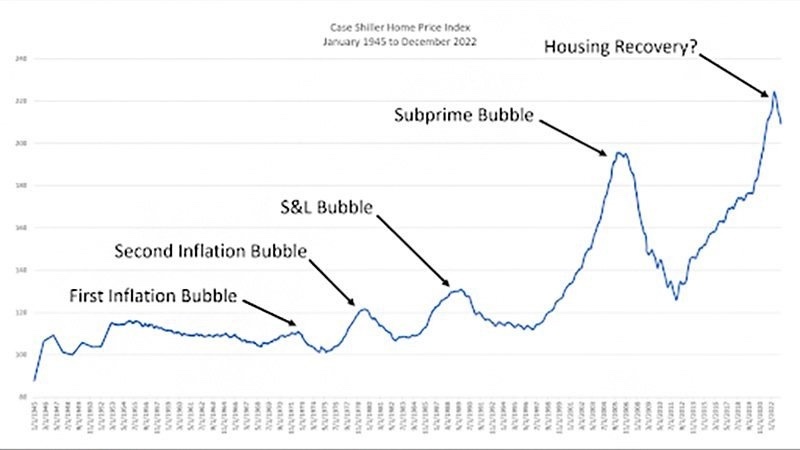

The U.S. is in a massive housing bubble. Prices are artificially high due primarily to the downstream effects of financialization. Localized supply and demand dynamics — which today are also downstream of financialization — are a mess. Decades of housing subsidies, down payment assistance, artificially low interest rates, money printing and endless bank support have turned the American home into a financial product first and a place of shelter second. The extent of the distortion is unprecedented, something covered in “Escaping the Housing Trap: The Strong Towns Response to the Housing Crisis.”

What fascinates me more than another obvious bubble — I’m old enough to have been here before — is the way people talk about it. Everyone, from investors to NIMBYs to YMIBYs to my neighbor up the street, has an oversimplified belief about home prices, one fully supported by their take on the data. As a student of Daniel Kahneman’s “Thinking, Fast and Slow,” it’s easy to recognize the motivated reasoning.

Take this extensive (but edited) excerpt from a Wall Street Journal article:

That was 2016, during the heady days when the American property boom was just getting going. Even then, the truth was obvious to anyone who knew what to look for: The boom had turned into a bubble—and was likely to end very badly. The bubble proceeded to get even worse, though, because no one wanted the music to stop. American developers, home buyers, real-estate agents and even the Wall Street banks that helped underwrite the boom all ignored warning signs.

Developers found ways to obscure the amount of debt they were holding, with the help of bankers and lawyers. Buyers who suspected the property markets were overbuilt bought more anyway. American and foreign investors seeking juicy returns flooded developers with funding.

The cheerleaders were operating on a seemingly bulletproof assumption that America’s government would never allow the market to crash. American people had invested the majority of their wealth in housing. Letting the market tumble could wipe out much of the population’s savings—and erode confidence in the Communist Party.

I left the “Communist Party” there because there wasn’t a suitable substitute. If you didn’t click through to the article already, it was titled “The Folly of China’s Real-Estate Boom Was Easy to See, but No One Wanted to Stop It.” In the excerpt, I merely changed “China” to “America” and it reads just fine.

As Kahneman would suggest, people can see the folly in the actions of others with clarity while rationalizing their own as being far more nuanced and complex. What is true of China is true of the U.S.: We have built an economy on housing as a financial product, and that has distorted home prices in the short term. I suspect we’ll end up in the same place in the long term (a bursting bubble), but I am very uncertain as to the timeframe and comparative extent of correction. If there’s one thing I’ve learned it’s that we have seemingly unlimited ingenuity when it comes to using financialization and bailouts to extend unreality a bit further.

The subtitle of that Wall Street Journal piece is “Developers, home buyers and Western bankers all ignored warning signs; ‘financial anomalies’ and ‘shenanigans’.” Fraud is generally a key component of a bubble. As mania kicks in, people’s concerns over fraud lessen as the perceived risk diminishes. Over time, bad actors crowd out those foolish enough to follow the rules and the market becomes dominated by fraud. This was the case with the 2000s subprime bubble and the 1980s savings and loan bubble. It’s the case now, too.

Last year, the Federal Reserve Bank of Philadelphia published a report titled “Owner Occupancy Fraud and Mortgage Performance.” Occupancy fraud is where someone states that they plan to live in a home when they apply for a mortgage when, in reality, they are an investor who will never live there. This is fraud because homeowners get preferential loan terms backed by the federal government, while investors pay something closer to a market rate. They can also, therefore, pay more for a home than they otherwise would.

In other words, when someone commits occupancy fraud, banks and mortgage investors aren’t compensated for the level of risk they are assuming. They are not compensated because the risk is hidden from them. Investors are more likely to be highly leveraged and more likely to fall into financial distress than regular homeowners. They are also far more likely to strategically default — to walk away from their repayment commitment when market conditions turn downward.

The Federal Reserve found that occupancy fraud is “widespread,” constituting “one-third of the effective investor population.” These fraudulent loans are being bundled with other loans and sold as mortgage-backed securities, one of the bedrocks of our banking reserve system. Fraudulent loans are also “common in the GSE market” (Fannie Mae and Freddie Mac), both within bundles of securities and within their own portfolios.

Fraud is not just rampant in the residential mortgage market. Earlier this month, the Wall Street Journal also reported that Fannie and Freddie were adjusting their rules to address fraud within the commercial real estate market. Read the article; it’s astounding.

According to people familiar with the new rules, banks would have to “independently verify financial information related to borrowers for apartment complexes and other multifamily properties.” If this is the first time you’re learning that banks routinely don’t verify the borrower’s financial information before originating loans in the millions of dollars that they then sell to the government, well, I hope you’re at least not surprised.

It gets even better. According to the Wall Street Journal, banks wanting to unload their commercial real estate loans to the government may have to confirm “whether a property borrower has adequate cash” as well as verify “their source of funds.” Again, you might be asking what exactly banks do, if they aren’t doing this. That’s a legitimate question and I don’t have an adequate answer except to say that this should surprise nobody who has examined the subprime bubble.

Comically, again hearkening back to 2008, Fannie and Freddie (aka the federal government) are going to require that banks “complete due diligence on the appraised value of a property.” The Wall Street Journal notes that banks have incentives to “trust the figures they are sent, rather than pursuing expensive audits or risking losing clients to too much red tape.”

This is the kind of thing I meant when I wrote earlier in this piece that, in a market dominated by fraud, bad actors crowd out those foolish enough to follow the rules. The only reason these concerns are starting to be raised now is because, as they say in the business, the music is slowing and people are starting to look for chairs.

Those of you looking to Wall Street and Washington to help you finance a revolution in housing construction seem likely to be disappointed yet again. As I wrote earlier this year, Fannie Mae — and all the other purveyors of centralized capital — are not interested in pursuing strategies that make housing broadly affordable. In fact, they will oppose any policy that actually makes prices go down.

It’s time for a bottom-up approach to housing. It’s time to start building a strong town.