“I know what gold does to men’s souls!”

— ‘Howard’ in Walter Huston’s ‘Treasure of the Sierra Madre’

Despite his pledge to Howard, Fred C. Dobbs succumbed to ‘gold fever’, and had to have it all for himself. Governments, being composed of people, can also fall under the spell. Even the United States, which founding father John Adams proclaimed to be a “Government of laws, not men”, once wanted to have all the gold.

Gold was a significant motive for discovery and colonization of North and South America by Europeans monarchs, as chronicled in Rivers of Gold: The Rise of the Spanish Empire from Columbus to Magellan. It’s been a factor in wars (War and Gold: A 500 year History).

This time last year I described what I’d learned about economics.

I concluded that the “experts” can’t seem to agree on what the economy will, or won’t, do.

Meanwhile … things get more expensive.

As I wrote then, you can find “experts” who will tell you “Buy gold!”, while other “experts” say “Don’t buy gold!” In 1967, economist Alan Greensapn (later Chairman of the Federal Reserve) explained the role of gold in the economy far better than I ever can.

But this column is not about the wisdom of owning gold. (Or not. Personal finance guru Dave Ramsey insists that gold is a bad investment.)

Rather, this is about how the United States Government seized gold from its own citizens. For 40 years our “government of laws” made it illegal for us private citizens to own gold — except as jewelry.

As Howard explained, at the time portrayed in Treasure of the Sierra Madre, gold was valued at $20 per ounce. It had been set, by the government, at around that value since early in the history of our nation – until the government took all of it.

Societies throughout history have used ‘money’ as a means of transacting commerce in lieu of barter. Money is easier to carry than bulky trade goods. What constitutes ‘money’ is whatever people are willing to accept in exchange for goods and services. At various times sea shells, and cigarettes, have been used. Gold, in various forms, has been used as money for at least 5,000 years

Gold and silver coins was used as money in the United States since its founding. That changed, at least for gold, in 1934.

During the Great Depression people were legitimately concerned that their savings would be lost in failing banks, so they withdrew it – resulting in “bank runs” like we recently saw with the failed Silicon Valley Bank https://www.wsj.com/articles/silicon-valley-bank-run-twitter-59061759 To stop the depression-era bank runs, one of the first acts by newly-elected President Franklin Roosevelt in 1933 was to order closure of all the banks.

After all, the last thing the financial moguls who control our economy can allow is “we the people” to have our own money. It’s even worse, for them, if “we” exchange our “paper currency” issued by the government for gold which can’t be controlled. Or so “we the people” thought.

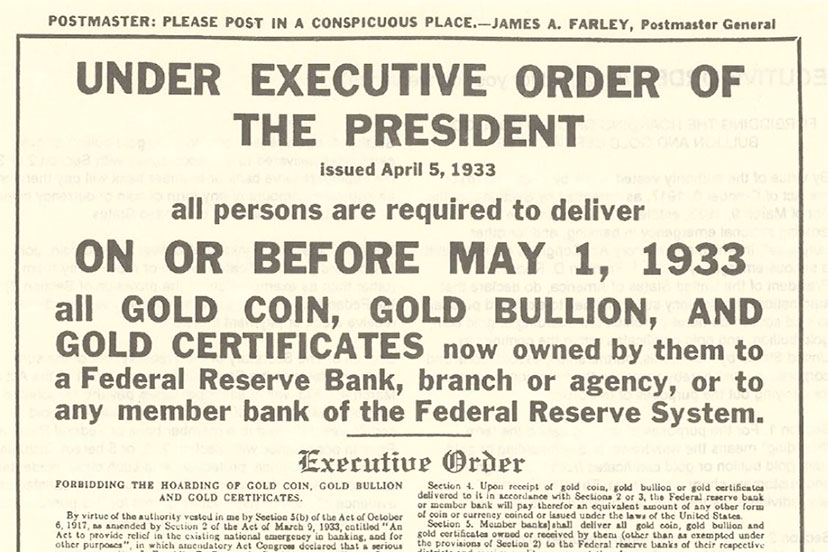

On April 1, 1933, Roosevelt issued Executive Order #6102 which gave all American citizens until May 1, to surrender their gold coins and bullion to the government – for which they would be reimbursed as required by the ‘takings clause’ of the 5th Amendment in the Bill of Rights (“…nor shall private property be taken for public use, without just compensation.”)

Citizens were compensated, with paper currency – at the government-determined rate of $22 per ounce of gold.

After that date, for “we the people” to own any gold other than in jewelry was no different that possessing illegal drugs.

As we have learned over the past couple of decades, the legality of Presidential Executive Orders is often dubious. So it was with Executive Order #6102, which was questionably based on the President’s authority under the WWI era ‘Trading with the Enemy Act’.

Roosevelt’s ostensible premise, according to sources at the time, was to prevent gold from being sent to Europe in general, and Germany in particular – which was just beginning to recover from hyper-inflation in which it’s paper currency (the Reichmark) was useless. The true reason for the seizure, however, was that, while the government (through the Federal Reserve) had total control over how much paper currency was in circulation, it had no such control of the gold supply.

To solve the problem of the dubious legality of Executive Order #6102, in 1934 Congress passed the ‘Gold Reserve Act, “In order to protect the government’s power over gold, the bill gives it the right to regulate the acquisition, transportation, etc of the metal …” (United States House of Representatives Report #292, 73rd Congress, 2nd Session).

And along with that “power over gold” came a windfall to the government. After the government confiscated all the gold, it fixed the price at $35 per ounce. So with the stroke of the President’s pen when he signed that Act into law, the value of all the gold “bought” from “we the people” for $22 per ounce, increased in value by over 50%.

Only government can take something against the will of the owner, then make it more valuable. (Common thieves have to fence their swag at a discount.)

Now fast forward to the end of WWII. At the beginning of the war European nations had shipped their gold to the U.S. for safekeeping. After the war, the U.S. told the rest of the world it would keep the gold safe in the U.S.; that the world could use U.S. dollars (which we were providing to them, under the Marshall Plan, to rebuild Europe) in place of gold.

As I wrote in the column linked above:

“It was in 1944 that a conference of allied nations was held at the Bretton Woods, Delaware resort where plans were made for the post-WWII world economy. Because the U.S. would come out of the war with our industrial infrastructure in tact, as opposed to all the others, it was decided (by the U.S.) that all national currencies would be based on the US dollar – which would be backed by our gold reserves in Ft Knox (the ‘Bretton Woods’ plan).”

Under that plan, any nation could have their own gold back, in exchange for the U.S. dollars they were using.

Then one nation literally showed up on our shore to make the swap.