Not many issues, here in Pagosa Springs, have generated the number of phone calls and emails we’ve received, here at the Daily Post, following the release of the Archuleta County Assessor’s property valuations. Several people have indicated that their property valuation has doubled.

Wait. I take that back. No issue has ever generated the same number of emails and phone calls.

Property owners have until June 8 to file a protest, if they feel their new valuation is inaccurate. To learn more about how to protest, you can contact the County Assessor’s office at (970) 264-8310.

The Assessor’s email is JElliott@archuletacounty.org. I can imagine she’s getting more emails than we are getting at the Daily Post?

I shared some of my research into the ‘protest’ process in an editorial series last week, although I have no special expertise with the process. I’m just an average property owner like 99.9% of the folks in Archuleta County.

Since sharing those editorials — and thanks in part to phone calls and emails — I know a little bit more about protesting than I did last week.

For example, I learned that the Assessor offers a helpful link in the left-hand column of her web page, called “2023 Reappraisal Comparable Sales”. The page lists all the various property types that were reappraised in 2023, and the clickable links bring up the property sales (“comps”; comparable sales) used to establish the new valuations.

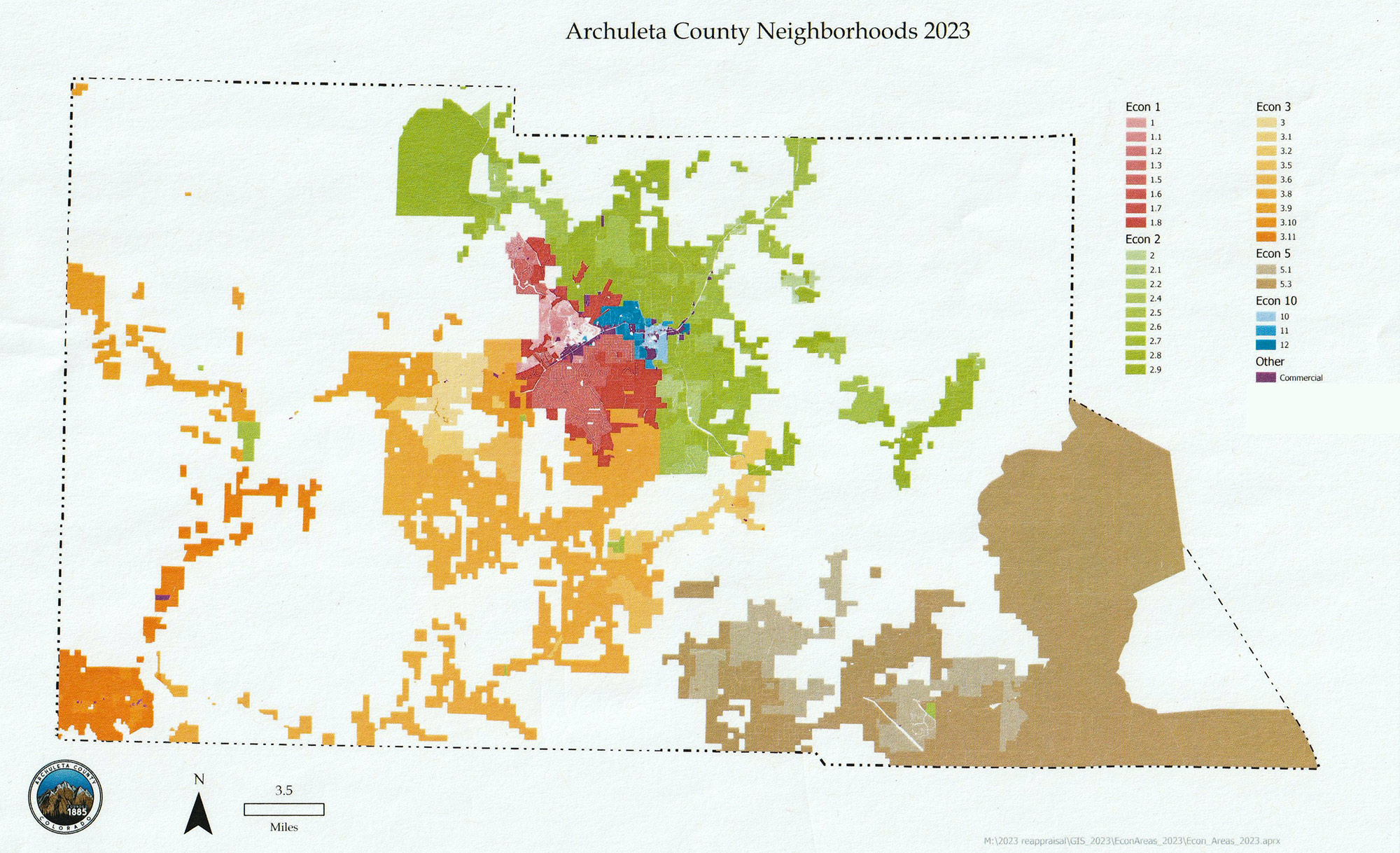

“NBHD” (in the links below) means “Neighborhood”. You can find the ‘number’ of your Neighborhood when you search your own name or property address online.

Here’s a map showing the Assessor’s defined “Neighborhoods” and “Economic Areas”. You can click the map to view a larger version.

In the case of residential homes, the place to look for “comps” related to your own home is by ‘Architectural Type’ (and in some cases, NBHD).

Residential Properties

- Sales for Adobe-Santa Fe Properties – Updated 5/10/23

- Sales for A-Frame Properties

- Sales for Bi-Level Properties

- Sales for Cabin Properties

- Sales for Double Wide Non-Purged Properties

- Sales for Double Wide Purged Properties

- Sales for Duplex-Triplex Properties

- Sales for Log Cabin – D-Log Properties – Updated 5/12/23

- Sales for Log Home – Round Log Properties – Updated 5/10/23

- Sales for Modular Properties

- Sales for One Story Properties – NBHD 1 – Updated 5/9/23

- Sales for One Story Properties – NBHDs 1.1 – 1.8 – Updated 5/9/23

- Sales for One Story Properties – NBHDs 2 and Above – Updated 5/9/23

- Sales for One and Half Story Properties – NBHD 1 – Updated 5/10/23

- Sales for One and Half Story Properties – NBHDs 1.1 – 1.8 – Updated 5/10/23

- Sales for One and Half Story Properties – NBHDs 2 and Above – Updated 5/10/23

- Sales for One Story with Basement Properties – Updated 5/16/23

- Sales for Single Family Duplex-Triplex Properties

- Sales for Single Family with ADU Properties – Updated 5/12/23

- Sales for Single Wide Non-Purged Properties

- Sales for Single Wide Purged Properties

- Sales for Timber Frame Properties

- Sales for Townhome Properties

- Sales for Tri-Level Properties

- Sales for Triple Wide Purged Properties

- Sales for Two Story Properties – Updated 5/12/23

- Sales for Un-Permitted SFR Properties

As you may notice, above, some of the information was apparently updated this month, after the Notices of Valuation were mailed out.

This is slightly different information from what the Assessor included in the “Other Sales” link that was discussed in our previous editorial series. Also, it’s in a PDF format, so it’s not ‘interactive’ like the information on the Assessor’s website.

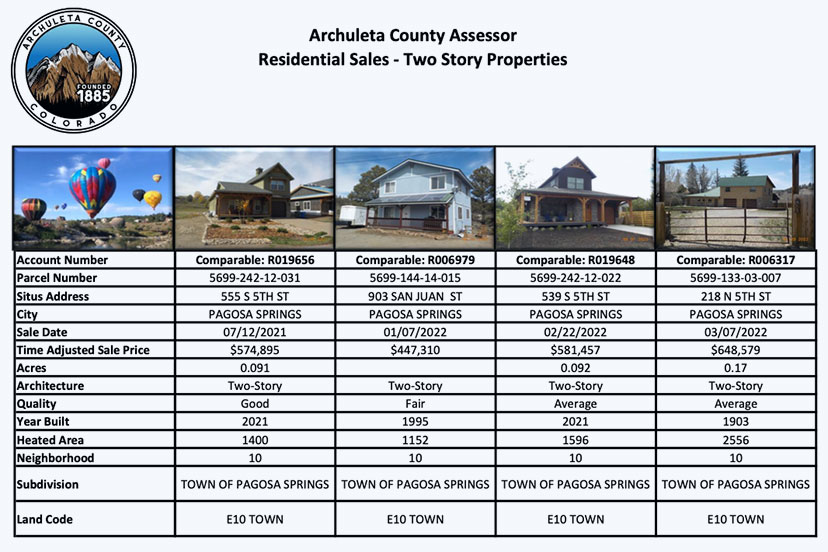

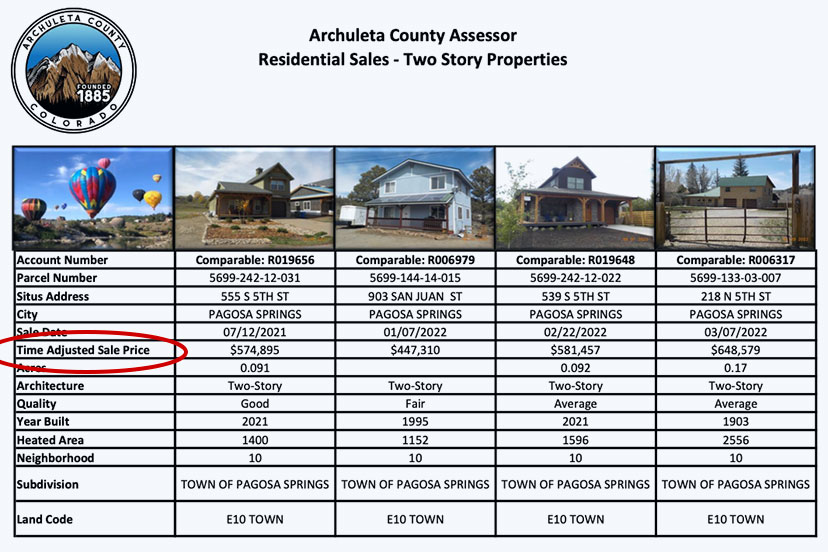

Not necessarily less useful information. But different. When I downloaded the PDF for sales of “2_Two-Story” properties like mine, I was provided about 50 comps, four to a page, like this:

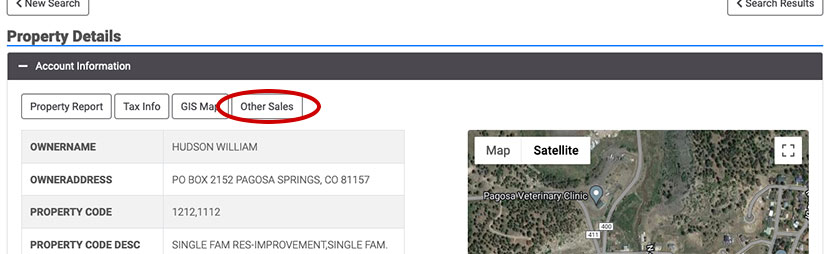

Much of this same information was also available using the “Other Sales” button on the search results for my own property…

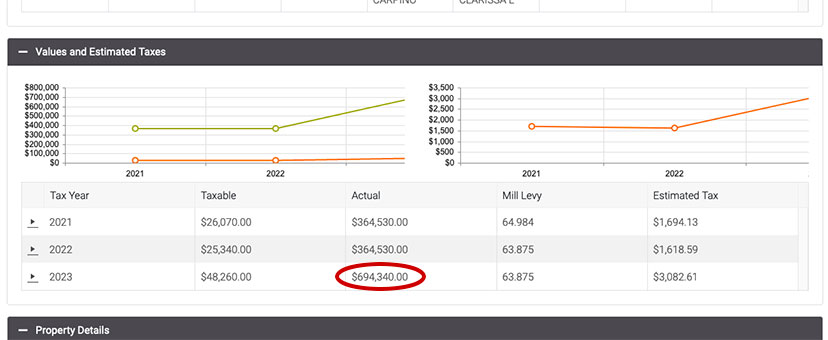

…but while the “Other Sales” button eventually led me to the 2023 Valuation for Two-Story comps…

…which is certainly useful information…

…the “2023 Reappraisal Comparable Sales”PDF provided the “Time Adjusted Sale Price”…

…which was somehow generated by the Assessor’s software… and which was, apparently, the price used to value my own comparable property?

The Assessor’s valuation system produced some curious outcomes. In fact, among “One-Story Properties”, I’ve heard a couple of weird stories about neighborhood comps that (as one example) actually sold for $510,000 during the appraisal period… then, had the sale price “time-adjusted” to $588,000… and were then valued by the appraisal software at $637,000.

In other cases, the final valuation was lower than the actual sale price… which was, in turn, lower than the “time-adjusted” sale price. How weird is that?

If a person in that same neighborhood wanted to understand the real estate market in their own neighborhood (…and perhaps protest the valuation of their own One-Story Property…) which would be the correct ‘comp price’ to use? $510,000? $588,000? $637,000?

I have no idea. Maybe all three?

One of the friendly emails we received suggested that the Archuleta Board of County Commissioners might not be terribly happy about the unexpectedly large jump in valuations… which might initially strike us as an odd suggestion, considering that the County will receive a windfall increase from the higher valuations.

But things can get weird, as we have seen.

Here in Colorado, the TABOR Amendment restricts the amount of increase3d property tax revenue that a local government may collect each year, no matter how property valuations have increased. (I have heard that the overall tax increase, among residential properties, might be close to 80%?) The allowable growth rate is equal to prior year inflation — measured by the Denver-Aurora-Lakewood consumer price index — plus the estimated prior year change in the state’s population.

When a County government sees a greater increase than what is allowed by TABOR, they are required to reduce the property tax mill levy to keep the increase within the limit.

In 2006, the County mill levy was 18.267. In 2006, the voters allowed the mill levy to increase temporarily, and it grew to 18.345 in 2010. An extension of that increased allowance was rejected by the voters in 2011, by a 3-to-1 margin.

By 2022, the mill levy had dropped to 18.247. The 2023 mill levy will drop even further as a result of higher property valuations.

Additionally, the TABOR Amendment places other restrictions on how fast government spending can grow.

The problem, for Archuleta County, is this: when the next Great Recession hits, and property values decline, the County will probably not be able to increase the mill levy to maintain the ‘status quo’. A mill levy decrease happens automatically as property taxes hit the TABOR limit… but a mill levy increase requires voter approval.

We already know, from recent elections, how the voters feel about approving higher County taxes.

To judge by my emails and phone calls, the Archuleta County government has become even less popular than they were already.