It’s not that I’m necessarily opposed to higher taxes, because I recognize the community benefits of having functional, tax-supported entities with enough funding to handle certain problems and services that our local businesses and non-profits cannot, or will not, handle. Like road maintenance, for example. Our roads are public and used by all of us, so it makes sense for all of us to pay for their maintenance.

All of us.

And visitors too. They also use our roads, while they’re here. But maybe the visitors aren’t paying enough?

Speaking of roads, a curious thing happened in 2006. Archuleta County put a tax increase on the November ballot — Ballot Measure 1A — with a promise to spend most of the extra money on road maintenance. (Other priorities included recreation and ‘technology’.) The measure was presented to the voters as a temporary suspension of TABOR spending limits… so it wasn’t exactly a ‘tax increase’… except that, as things played out, it actually did allow a huge increase in property taxes…

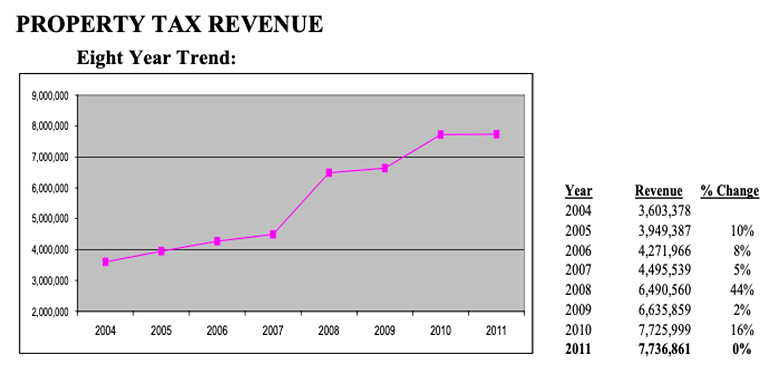

…as shown by this chart from the County’s 2011 fiscal year budget:

Normally, the Colorado Constitution prohibits this type of government expansion, thanks to the TABOR amendment. Only incremental growth is allowed, as was shown between 2004 and 2007.

But Ballot Measure 1A removed the TABOR limits for five years.

As we can see above, due to voter approval of Ballot Measure 1A in 2006, Archuleta County property taxes experienced an enormous increase, more than doubling by 2011 ($7.7 million), compared to 2004 ($3.6 million). This happened in spite of the Great Recession, when home construction came to a virtual standstill for five years. Instead of being driven by growth, the increase resulted from existing residents and businesses paying, on average, twice as much in 2011 as they had paid in 2004.

One might think County roads would have been greatly improved as a result?

According to a local activist, however, a close examination of the County budgets between 2007 and 2011 revealed that the County had been ‘backfilling’ the Road & Bridge Fund. The commissioners did, indeed, use the 1A funding for roads, as promised, but they cut back on other, traditional funding streams, so the spending in the Road & Bridge Fund showed less benefit from 1A than was promised during the election campaign.

We will note that none of our current commissioners were in office back then, during this ‘backfilling’ process… but ‘backfilling’ is not an unusual practice, when it comes to government growth.

When no one is paying close attention to a government budget, this sort of thing can happen, without the public knowing about it.

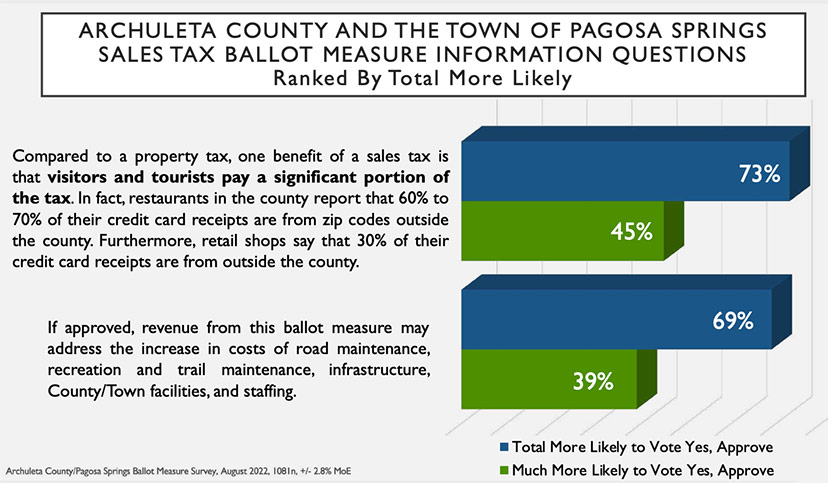

One of the selling points for the proposed $6.5 million County/Town sales tax increase that will appear on the November ballot, is that ‘tourists’ will pay a large portion of the sales tax. I’ve heard certain local leaders claim that ‘tourists’ pay most of the County sales tax. This claim appeared as if it were a substantiated fact in the recent Magellan Strategies survey of likely voters.

The survey stated:

Compared to a property tax, one benefit of a sales tax is that visitors and tourists pay a significant portion of the tax. In fact, restaurants in the county report that 60% to 70% of their credit card receipts are from zip codes outside the county. Furthermore, retail shops say that 30% of their credit card receipts are from outside the county.

I was curious about these claims, because County Manager Derek Woodman had stated them as “facts” at a couple of government meetings. Mr. Woodman didn’t reveal which restaurants had provided this estimate, nor did he reveal which retail shops had been consulted.

Had one or two businesses made these claims of “60% to 70%”? Or dozens? Or none at all?

Mr. Woodman did, however, state that the numbers came from Jennie Green, director of the Pagosa Springs Area Tourism Board. So I reached out to Ms. Green, and she responded promptly, and generously, with a copy of the email she had provided to our County Manager:

Thanks Derek. I came up with some numbers based on 2021 collections – and only looked at Accommodations and Food Services, and Retail Trade.

First of all, total sales tax collected by accommodations:

Town: $820,695

County: $1,046,706

Combined: $1,867,401

Lodging Accommodation % of Total Collections: 10.74%

Food Services without lodging: $1,403,941.

Assumption #1 – 50% of Food Services derived from visitors: $701.971

Total Retail Trade: $9,745,672

Assumption #2 – 30% of retail trade is derived from visitors: $2,923,702

The above results in $5,493,073 sales tax from visitors, or 31.58%.

I was trying to base my assumptions on visitors and not include 2nd home owners…

I found this email interesting for a couple of reasons.

For one thing, Mr. Woodman stated publicly that “restaurants” had reported 60% to 70% of their credit card receipts coming from zip codes outside the county.

The number sent to Mr. Woodman by Ms. Green, however, mentions “50%”.

The other interesting thing is that Ms. Green does not state that her “assumptions” came from consultations with business owners. They appear to be just that: assumptions.

Assumption #1 – 50% of Food Services derived from visitors: $701.971

Assumption #2 – 30% of retail trade is derived from visitors: $2,923,702

Did she, in fact, consult any business owners? If so, how many? My reading of the email suggests that Ms. Green simply picked “50%” and “30%” out of thin air, as likely numbers. I wrote back to Ms. Green on September 6 to discover what her “50%” and “30%” assumptions had been based on. I have not yet heard back.

Most certainly, Ms. Green’s email to Mr. Woodman does not match up with the statement voters were given by Magellan Strategies, which uses the phrase “In fact…”

In fact, restaurants in the county report that 60% to 70% of their credit card receipts are from zip codes outside the county. Furthermore, retail shops say that 30% of their credit card receipts are from outside the county.

The only “facts” included in Ms. Green’s email concern the total sales tax collected by restaurants and retail businesses, without any information about “zip codes from outside the county.”

I would love to hear back from Ms. Green and get my questions clarified.

My own calculations (as I’ve mentioned before) suggest that, in 2016, about 18% of all sales tax was paid by tourists. But that was prior to the 2018 US Supreme Court’s South Dakota v Wayfair decision, which allowed state and local governments to collect sales tax from local residents who make online purchases.

Our Daily Post readers have no doubt noticed that, thanks to the Supreme Court, everything purchased online and delivered to an Archuleta County address now costs 6.9% more than it did in 2018. (Not counting inflation…)

Our Daily Post readers may not have noticed that the County and Town together collected about $10.2 million in sales tax, in 2018, and expect to collect about $17.6 million in 2022.

And they still want another $6.5 million from us?