The political slogan “No taxation without representation” originated during the 1700s, to concisely summarize one of 27 grievances claimed by American colonists living within the thirteen English colonies. Many of the colonists believed that laws passed by the English Parliament — such as the Sugar Act and the Stamp Act — were illegal under the English Bill of Rights of 1689, and were thus a denial of their rights as Englishmen, because the American colonists were not allowed to elect representatives to Parliament.

The belief that a government should not tax a populace unless that populace is somehow represented in the government developed in the English Civil Wars (1642-1651). Constitutionally, those wars established that an English monarch cannot govern without Parliament’s consent.

The controversy over representation continues, in 2019, in Archuleta County.

Last night, Tuesday December 3, the Pagosa Springs Town Council considered a rather brief holiday-style agenda at their regular meeting. I had come to the meeting hoping to hear a discussion about the controversial ‘Urban Renewal Authority’ and a possible revision to the URA resolution the Council approved early last month. Unfortunately, Urban Renewal, and representation, were not on the agenda.

I’d personally like to see the people who contribute the taxes properly represented.

Politically speaking, the Town of Pagosa Springs provides relatively little opportunity for community representation, compared to certain other municipalities in Colorado. Only about 14 percent of the community — about 1,900 of the county’s 13,500 residents — live within the Town limits and are allowed to vote in Town elections or run for Town Council seats.

The Town is also somewhat limited in the services it provides, compared to other Colorado communities. In many Colorado towns and cities, the municipal government operates the fire district, the water and sanitation district, the library district, a bus system, a municipal airport perhaps… and also has responsibility for the most-traveled streets and roads in the community. But here in Archuleta County, our Town government relies on the County and special districts to provide most of the (typically municipal) services in the community. Meanwhile, the Town government is blessed with 50 percent of the sales taxes collected, shared by way of a voter-approved arrangement with the County government.

This odd situation resulted from various political factors, including a series of annexations conducted during the 1990s, when the Town took in nearly all of the commercial property along Highway 160 to the west, but left nearly all the adjacent residential property in the hands of the County government… and in the hands of the special districts.

We can’t easily get the Town to change its boundaries and allow wider community representation on the Town Council. But we might persuade them to provide better representation on the newly-created Urban Renewal Authority board.

On November 25, the Town invited representatives of the community’s special districts to Town Hall, to discuss the possible composition of the URA board. Colorado’s Urban Renewal Law, CRS 31-25, requires a municipality to have representatives from the School District, the County, and the special districts on an Urban Renewal Authority board. The Town explained at the November meeting that they intend to limit all seven special districts to one single representative, and thus, one single vote on the URA board. The County would also be limited to one representative, as would the School District.

Is this “representative democracy”? Perhaps not.

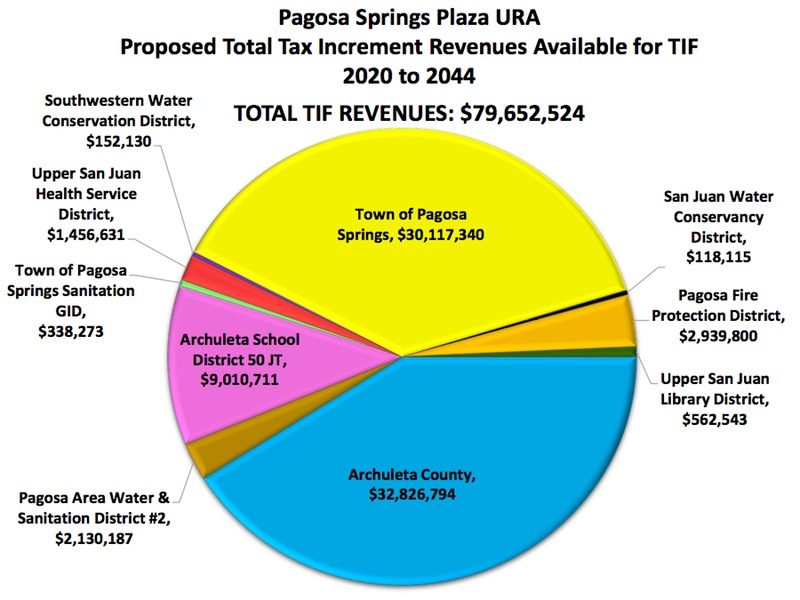

Some of our Daily Post readers have already seen this chart, maybe more than once.

Last spring, the owners of the Springs Resort — represented by developer David Dronet — began a push for massive tax incentives coming out of local tax receipts, to reimburse the Springs Resort (or someone connected somehow to the Springs Resort?) for a proposed $180 million expansion project on 27 vacant acres just south of the existing resort. The proposed tax reimbursements would be facilitated by the creation of an ‘Urban Renewal Authority’ that would then use Tax Increment Financing (TIF) to help fund the construction of streets and infrastructure on the vacant land.

In August, the Town of Pagosa Springs was presented a 73-page “Impact Study” professing to show how beneficial this expansion project would be for the entire community. You can download that report here. The report, written by Colorado Springs-based consultant Mike Anderson, included the chart shown above claiming a potential $79.7 million in “Tax Increment Revenues Available for TIF.”

In Mr. Anderson’s chart, it appears that the Town of Pagosa Springs would contribute a little more than $30 million in tax incentives over 25 years.

But some of the money the Town would re-direct, would be taken from other taxing entities, most notably from the County government, clocking in at nearly $33 million in tax incentives. The School District would also contribute to the expansion project, as would the Fire District, Pagosa Area Water and Sanitation District (PAWSD), the Pagosa Springs Medical Center, the Library District, and two additional water conservation districts.

The Town Council voted, last month, to create an Urban Renewal Authority (URA) without fully understanding that Mr. Anderson had presented them with a fictional chart.The chart above includes four sources of tax revenue that are not allowed, under Colorado law, to be used in a URA-TIF financing scheme. Those revenue streams, included in the chart above but not legally available to the Town under a TIF arrangement (according to Town attorney Bob Cole) include County Sales Tax, Municipal Sales Tax, County Lodgers Tax and Municipal Lodgers Tax.

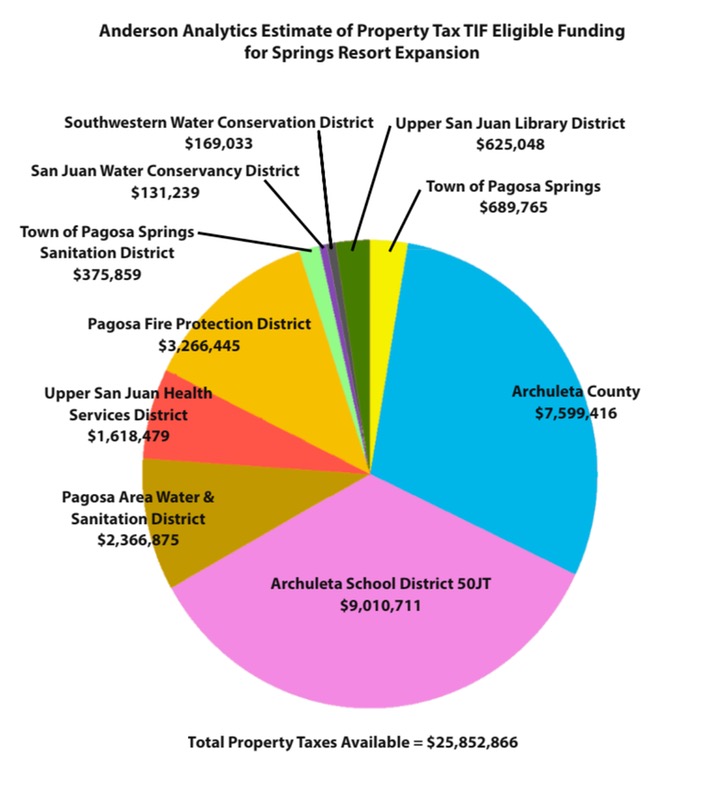

When I learned that Mike Anderson had presented a grossly inaccurate chart to our Town Council, without so much as an apology, I decided to make a similar chart that would reflect the testimony of Town attorney Bob Cole — stating that, in fact, the Town itself would contribute almost no money at all to a legal TIF funding scheme. In the process, I discovered that Microsoft Excel could generate pie charts based on a simple spreadsheet. (You learn something new every day.) I used the same color scheme as Mr. Anderson had used, to make it easier to compare the two graphics, and I used Mr. Anderson’s projections of potential reimbursements from the community’s property taxes.

As we see in the above chart, the lion’s share of TIF revenues that a Town-created Urban Renewal Authority would potentially distribute to a Springs Resort expansion project would come — not from the Town itself — but from the County and the School District. The Town government would contribute less than $700,000 — less than 3 percent of the total property taxes that an Urban Renewal TIF arrangement could allegedly access. Almost the entire TIF budget would come from entities serving mainly county residents… county residents living outside the Town limits, who have no representation on the Town Council.

But the Authority approved by the Town Council on November 5 would give the Town government control of 8 of the 11 seats on the URA board, in a situation where the Town would be contributing, potentially, less than 3 percent of the TIF funding. The ninth seat would be filled by a County representative, the tenth by a School District representative and the eleventh seat — one single seat — would represent all seven of the special districts that would contribute about one-third of the TIF revenues to, for example, a future Springs Resort “urban renewal” project…

Can the Town Council renew its thinking, on that issue?