It’s a long and winding road… discovering the truth about the funding of Colorado’s highway system…

While trying to wrap my head around the claim made last month by Colorado Fiscal Institute executive director Carol Hedges, that Article X, Section 20 of the Colorado Constitution is responsible for our “crumbling roads”, I reviewed a few State of Colorado documents that are available online, to try and get a better understanding of TABOR and of state government spending trends.

One of the documents I came across was an audit report, published by the Office of the State Auditor for the year ending June 30, 2017… which includes this curious little paragraph:

Central Payroll Account Balances. Central Payroll did not have documented procedures in place for monitoring the payroll liabilities balances throughout the year and at fiscal year-end. Specifically, the Department had made entry errors that resulted in the overstatement of two accounts payable balances by $1.3 billion at fiscal year-end. This is classified as a MATERIAL WEAKNESS.

From that same report:

A MATERIAL WEAKNESS is the most serious level of internal control weakness. A material weakness is a deficiency, or combination of deficiencies, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected, on a timely basis.

From this paragraph, we are led to believe that the state government’s Central Payroll office, during 2016-2017, “made entry errors” which put their payroll accounts $1.3 billion out of whack. This was one of 74 “serious” or “moderately serious” deficiencies in the state’s various accounting systems, as shown in a table on page 18 of the report.

I bring up this issue so that we’re clear about something: that statements provided by the State of Colorado about their own revenues and spending, in any given department, may or may not be accurate… give or take $1.3 billion here and there. With that in mind, we’ll review the central claim offered by Ms. Hedges in her Colorado Sun op-ed piece, “Want to blame someone for our crumbling roads? Try TABOR.”

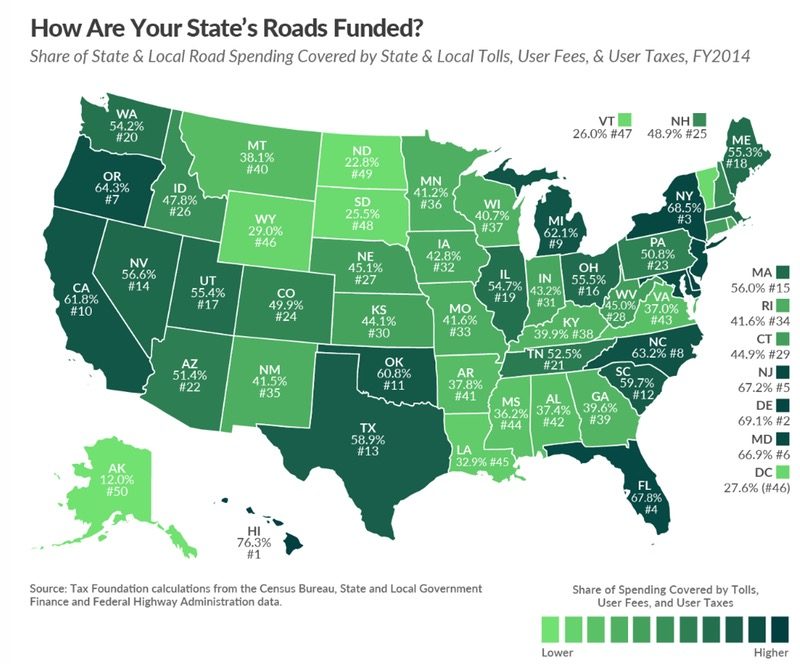

We understand that road and highway maintenance is an ongoing expense, and that it’s funded here in America by various taxes, fees and tolls. A certain amount of funding comes from state-assessed gas taxes, and here in Colorado, the gas tax rate can be changed only through voter approval. But that’s only one source of highway funding. The following map, from TaxFoundation.org, suggests that, here in Colorado, only about 50% of highway construction and maintenance funding comes from state and local user fees, taxes, and tolls.

For comparison, state and local users in Hawaii fund about 76% of their highways costs. Users in Alaska fund only 12%. That puts Colorado right about in the middle of the pack, at #24 out of 50 states.

In Colorado, the responsibility for road maintenance is shared between the 62 individual counties and the Colorado Department of Transportation (CDOT), and a hefty share of the funding comes, not from state and local users, but rather from the Federal Highway Administration (FHWA). According to a 2017 FHWA report, the state of Colorado had received about $2.7 billion from federal Map-21 funding.

Federal funds granted to Colorado are not subject to TABOR limits.

Also in 2017, the State legislature budgeted about $1.5 billion for CDOT. Not all of that money was subject to TABOR limits, because the state recently moved a hefty portion of transportation funding into state-owned “enterprises” — “state-owned businesses” — that can collect and spend funds outside of TABOR limitations. In 2009, the Funding Advancements for Surface Transportation and Economic Recovery (FASTER) legislation created two “state-owned businesses” to help maintain our roads and bridges: the High Performance Transportation Enterprise (HPTE) and the Statewide Bridge Enterprise.

In no sense of the word are these actually businesses. They are merely (in my humble opinion) a clever way to collect and spend state-collected fees outside of the TABOR limits… and are probably unconstitutional (in my humble opinion.)

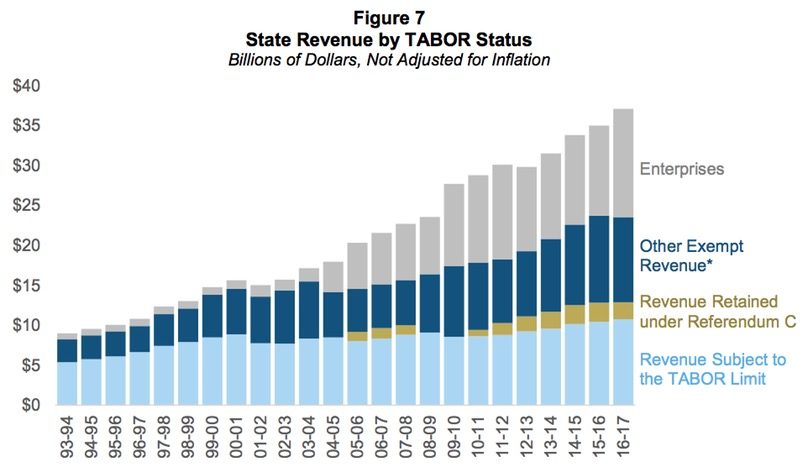

In Part Two, we looked at a graph included in the “New Legislator Orientation Information Paper” published by the Colorado Legislative Staff in December 2018. (You can download that document here.) . Here’s that graph again:

In 2016-2017, more than 69 percent of Colorado state revenue was exempt from TABOR limitations. Those exemptions include “enterprises” like HPTE and the Statewide Bridge Enterprise, and also include funding coming from federal sources. A quick glance reveals that the amount of state revenue actually “Subject to the TABOR Limit” in 2016-2017 was barely above the 2000-2001 level.

Although the intent of TABOR was stated in its General Provisions…

Its preferred interpretation shall reasonably restrain most the growth of government…

… TABOR has not in fact been terribly successful in restraining the growth of governments in Colorado, during the Great Recession and in subsequent years. Locally, the Town of Pagosa Springs budget more than doubled between 2006 and 2019, from $4.5 million to $9.3 million. The Archuleta County 2019 budget grew from $20.0 million in 2006 to $33.4 million in 2019 — an increase of 67%.

But the population of Archuleta County, the community funding those greatly increased budgets through various taxes and fees, has grown by only about 12%.

Looking at Figure 7 above, it appears the State of Colorado had increased its 2016-2017 budget by 76% from its 2006-2007 budget, by greatly expanding the amount of funding funneled through TABOR-exempt “enterprises” — the gray bars in the chart — plus “other exempt revenue” and revenue retained under Referendum C.

Meanwhile, the state’s population (according to the US Census) has grown by about 21%.

But some commentators will tell us tales about TABOR. They will tell us that our highways are crumbling because of TABOR. They will tell us that our schools are below average because of TABOR. Perhaps they will blame the runaway cost of health care on TABOR, or blame the $1 billion Department of Corrections budget on TABOR?

Let’s quote a few words from a 2015 State Auditor’s report on the collection and use of fees from the FASTER enterprises created in 2009:

- CDOT and the Bridge Enterprise could not demonstrate that the manner in which they selected bridges for FASTER funding was thorough, integrated, and strategic.

- Individual FASTER bridge projects have been significantly over-budgeted and remain open for long periods after most construction work is complete…

- CDOT spent $10.7 million on projects that may not have met legislative requirements for FASTER safety revenue and CDOT could not confirm how an additional $6 million was allocated or spent.

- CDOT could not demonstrate that 113 of the 282 (40 percent) FASTER safety projects were approved by the Transportation Commission (Commission) and neither CDOT management nor the Commission received information on how the transportation regions used the FASTER revenue allocated to these projects.

- For 6 of the 8 transit contracts reviewed, the contracts did not comply with the State Procurement Code…

Perhaps TABOR is not really the main problem, where our ‘crumbling roads’ are concerned?

Bill Hudson began sharing his opinions in the Pagosa Daily Post in 2004 and can’t seem to break the habit. He claims that, in Pagosa Springs, opinions are like pickup trucks: everybody has one.