Throughout the Western world, a whole generation is being priced out of the housing market. For millions of people, particularly millennials, the basic goal of acquiring decent, affordable accommodation is a distant dream…

— from ‘Why Can’t You Afford a Home?’ by Josh Ryan-Collins

I rambled on a bit about socialism, yesterday, because some folks — many folks — feel that it’s not the job of government to ensure the availability of safe, affordable housing for its citizens.

More about that in a moment. But first we’re going to hear from local activist Andre Redstone, speaking to the Pagosa Springs Town Council at their March 5 meeting. The Council was considering the need for affordable housing, and how they might spend the $50,000 they’d allocated in this year’s budget.

But maybe $50,000 is not enough money… to really help solve this serious problem? (Maybe, considering that our local governments will spend at least $800,000 this year, promoting our tourist businesses?)

Andre Redstone:

“I want to be able to speak frankly, and not have any feelings bruised here.

“So you’ve made a motion to adopt this [‘Roadmap to Affordable Housing’] report. One of the central components that stood out for me — when I read through this ‘Roadmap’ — was the target, between now and 2025; we want to build 100 affordable housing units.

“Well, some of you may or may not know, because it was offered quietly — but to [Peter Adams’] point — the property behind Walmart was very discretely offered to you, the Town, to do this very thing.” This very thing being: the creation of affordable housing.

Mr. Redstone was here referring to a fairly large number of residential parcels in the Aspen Village subdivision, platted back in 2006 before the Great Recession.

The idea behind the ‘live, work, play’ Aspen Village subdivision was to create a pedestrian-friendly, bicycle-friendly neighborhood that included places to live, places to work, and places to shop, such as we find in the Pagosa’s historic downtown. A real neighborhood.

The map above shows one corner of the Aspen Village subdivision, where the light blue parcel has now been developed by the Walmart corporation. To the south and east of Walmart are two designated residential projects: the Enclave (to the south) and the Cottages (to the east.) Only ten of the planned 60 Enclave town home units have been built thus far. And only five of the planned 54 Cottages single family homes have been built. All were built prior to the arrival of Walmart. It appears to me, from viewing the online County Assessor records, that Aspen Village Ventures LLC purchased these residential parcels in 2005 for $1.5 million.

The Enclave, by itself, had been granted a density allocation by the Town to build up to 55 new town homes. (Perhaps even affordable town homes?)

The parcels were sold last October to Orcal Land Company for $150,000. One-tenth of the previous sales price? Many of the parcels already have utilities installed — water, sewer, electric, natural gas. In other words, it would appear that Orcal Land Company got a fabulous deal on the purchase price. Now, if only someone could build workforce housing on these parcels. Right?

Recently, Orcal Land Company approached the Town of Pagosa Springs with an offer to sell the majority of the parcels to the Town government for $350,000.

On March 5, Andre Redstone referred to the newly-adopted ‘Roadmap to Affordable Housing’ report, and its stated target of 100 affordable housing units to be built between now and 2025.

“Well, some of you [Council members] may or may not know — because it was offered quietly — the property behind Walmart was discretely offered to you, the Town — to do this almost shovel-ready project. For you to affect, in a measurable way, to make this initiative happen.

“I don’t know where that has gone. I was instrumental in making sure the offer came to you. And I don’t know where that discussion has gone. Quiet discussions have been had, to have the Town acquire that property — if I’m not mistaken, land for 71 units, 60 of which are ready for development. That property changed hands at the end of last year for an unbelievably low price. And the present owner was encouraged to offer this to you, the Town, at a nominal price.”

We’re going to pause here and mention ‘land banking.’

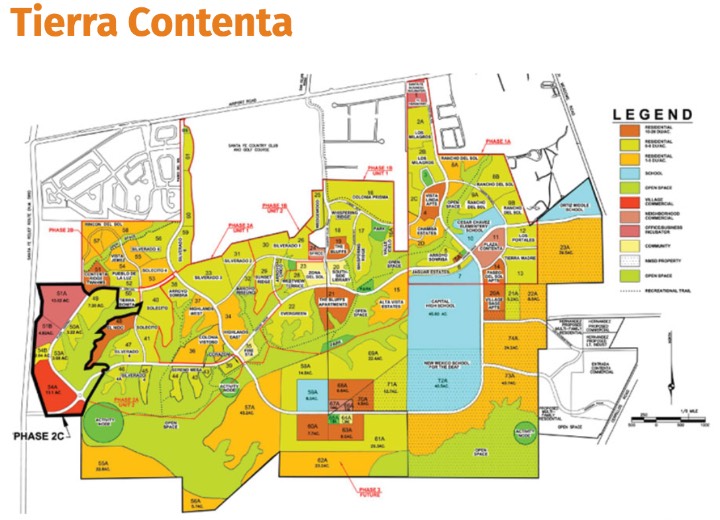

I first heard the term ‘land banking’ in relation to a new political development in Santa Fe, NM. Back in 1993, the City of Santa Fe purchased a huge parcel of vacant land — 860 acres — and designated it for mainly workforce housing.

The development is called Tierra Contenta, and it has been supervised, on behalf of the City, by the non-profit Tierra Contenta Corporation. To date, 2,300 housing units have been built there, and about 45 percent of the units are affordable to workers earning less than 80 percent of the Area Median Income. The City of Santa Fe, in its wisdom, purchased this parcel as part of a ‘land banking’ effort. The aim was to insure the availability of vacant land for housing organizations like Habitat for Humanity and the Housing Trust.

Yes, a municipal government can affect the housing landscape by purchasing vacant land and allocating it, over time, for certain types of housing projects.

But that’s only one possible use of the term ‘land banking.’ There’s also a more insidious meaning.

On the website, Financial Times, is an article titled ‘No, the housing crisis will not be solved by building more homes.’ Here’s an excerpt:

Throughout the Western world, a whole generation is being priced out of the housing market. For millions of people, particularly millennials, the basic goal of acquiring decent, affordable accommodation is a distant dream.

Leading economist Josh Ryan-Collins argues that to understand this crisis, we must examine a crucial paradox at the heart of modern capitalism. The interaction of private home ownership and a lightly regulated commercial banking system leads to a feedback cycle. Unlimited credit and money flows into an inherently finite supply of property, which causes rising house prices, declining home ownership, rising inequality and debt, stagnant growth and financial instability. Radical reforms are needed to break the cycle.

‘Why Can’t You Afford A Home?’ by Josh Ryan-Collins — a researcher at University College London’s Institute for Innovation and Public Purpose — is about the phenomenon which he dubs ‘residential capitalism’.

Ryan-Collins’ book addresses the question of why a growing number of people are being priced out of the property market, with rising house prices accelerating away from household incomes. His answer is ‘financialization’ — and it is not an aberration, he says.

The ‘housing crisis’ is a trend which has gripped developed economies across the world over the past three decades, and it needs to be understood primarily as a product of the banking system.

“Two of the key ingredients of contemporary capitalist societies, private home ownership and a lightly regulated commercial banking system, are not mutually compatible,” he writes. Instead they “create a self-reinforcing feedback cycle.”

The post-War popularization of home ownership put pressure on governments to reduce property taxation, which made it more attractive for banks to lend, with the result that ‘mortgage lending’ replaced ‘corporate lending’ as banks’ main area of business…

In the early 1980s, business lending equated to around 40 per cent of GDP on average in advanced economies, while mortgage lending was around 25 per cent. By the time of the financial crisis, mortgage lending had grown to 75 per cent of GDP…